Milk, Dairy and Grain Market Commentary

- Monica Ganley

- Jul 12, 2024

- 4 min read

By Monica Ganley, Quarterra Monica.Ganley@QuarterraGlobal.com

Milk, Dairy & Grain Markets

Soaring temperatures and suffocating humidity are challenging milk production in many parts of the country. As the mercury rises, cow comfort has suffered and milk production has declined. Spot milk availability has tightened up considerably and Dairy Market News notes that even during the holiday last week, milk handlers in the Midwest had few excess loads to place. Processors that hope to find spot loads of milk are paying an average of 50¢ over Class III – a sharp contrast to the five-year average of nearly a $2.70/cwt. discount.

The weather is further exacerbating tightness in the U.S. milk supply which has trailed prior year levels on a liquid basis for almost a year. However, the tables may be turning as margins have improved considerably in recent months. The May Milk Margin Over Feed Cost reported by USDA as part of the Dairy Margin Coverage program reached $10.52/cwt. in May, up 92¢ from April and the highest figure since November 2022. But despite the dramatic increase in margins, producer expansion remains constrained by elevated interest rates, heifer scarcity, and high beef prices which are stymieing dairy herd growth.

Limited milk supplies have been most prominently felt by dryers, who have not demonstrated the strong production that would typically be expected early in the year. Combined production of nonfat dry milk (NDM) and skim milk powder (SMP) in May was down 15.9% year over year and cumulative production of NDM/SMP during the first five months of 2024 is the lowest it has been in a decade. Yet, despite weak milk powder production, NDM prices at the CME have remained remarkably stable, trading in just a 20¢ range over the last 17 months. The NDM spot price ended this week unchanged from last Friday at $1.18/lb., as 14 loads traded hands.

Price stability has been a product of tepid demand balancing out weak supply. May exports of NDM and SMP tumbled to just 133.6 million pounds, down 24.2% year over year and representing the lowest value for the month since 2017. Slower demand from Mexico has been a key driver of the decline as cumulative shipments south of the border have fallen 18.3% this year. Mexico has not been fully responsible for the dip, however, as shipments have also slowed markedly to key destinations in Southeast Asia, among others.

The story is significantly more inspired on the other side of the Class IV complex, where butter prices persist at high levels. After a 6¢ jump on Monday, spot butter gave up ground on Thursday and Friday, ending the week down a penny at $3.10/lb. - still a remarkably strong price by historical standards. Butter demand remains upbeat, even at current levels. However cream supplies have tightened considerably with the summer heat and churns report that increased competition from Class II users are introducing more tension into the cream market. Butter production rose 4% year over year in May, but the current market seems to insist that it wants more butter.

Cheese production also expanded in May, rising 0.7% compared to the same last year. However, the increase was driven almost entirely by rising output of Italian varieties, which leapt 4.4% compared to the same month last year. Meanwhile, Cheddar production during May tumbled 9.7% year over year with a lack of available supplies likely giving the spot market the fuel it needed to run toward $2/lb. during the month. Cheese exports surged in May with 105.9 million pounds shipped during the month, second only to March’s all-time high figure. Record cheese exports to Mexico and stronger volumes to Korea bolstered the overall May figure. However, the cheese that shipped during May was probably booked several months earlier when prices were significantly lower. The higher cheese prices we are seeing today, which have largely converged with other international suppliers, will likely dampen the pace of cheese exports in the coming months.

The cheese markets wavered at the CME this week as gains early on were canceled out by losses on Thursday and Friday. Cheddar blocks added 7¢ between Monday and Wednesday before giving up the gains and ending the week at $1.89/lb., down one cent from last Friday. Barrels were softer yet with a 3.75¢ gain on Monday wiped out by 9¢ of losses late in the week, bringing the price to $1.85/lb. as 31 loads traded hands.

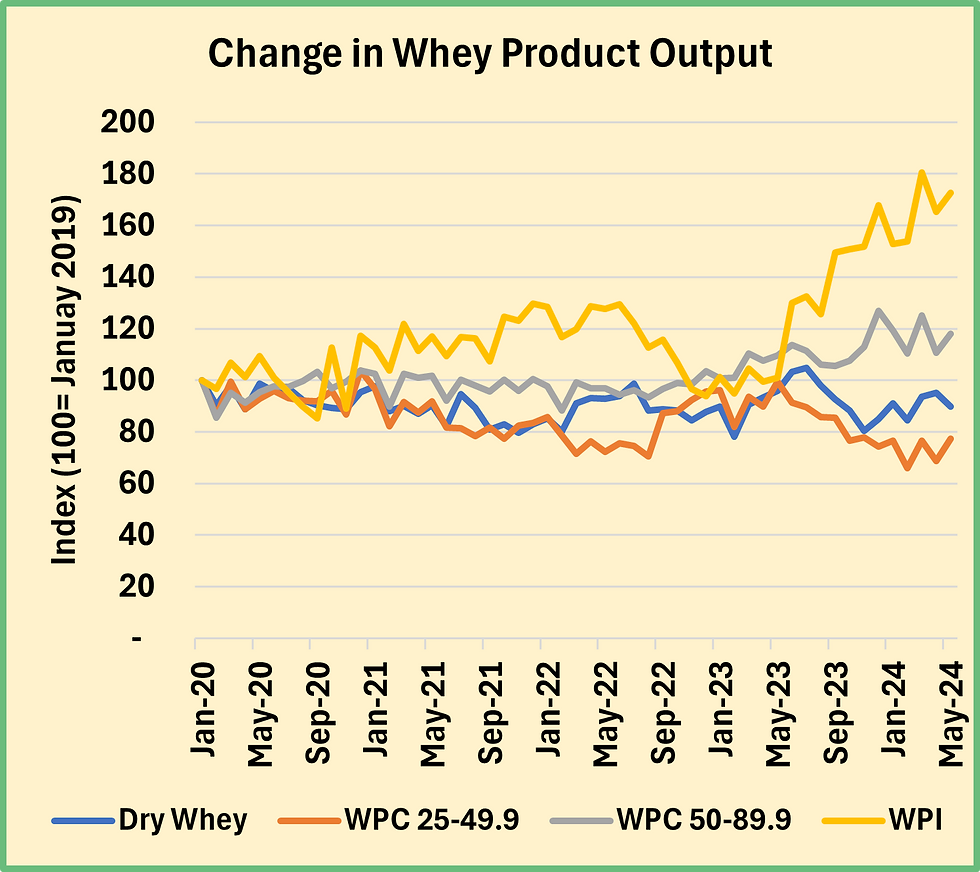

Whey markets found the motivation this week to break through the 50¢ per pound threshold for the first time since February. After a small dip on Monday, the market bounced back and added price on Tuesday and Thursday. Dry whey ended Friday’s spot session at 51¢ per pound, up 1.75¢ from last week with 3 loads moving. Whey production has remained perky as consistent cheese production has created an ample whey stream. However, manufacturers continue to show a distinct preference for value added products like whey protein isolates and high protein whey protein concentrates. As a result, the portion of the whey stream routed to dry whey production remains limited and is likely to keep prices supported in the near term.

Grain Markets

USDA released the July World Agricultural Supply and Demand Estimates report today. Corn production estimates for 2024/25 were increased by 1.6% on acreage gains. However, a reduction in beginning stocks and an increase in use and exports pushed ending stocks down. In the soybean balance sheet, a modest decrease in acreage pulled the production forecast down by 0.3%. Lower output combined with slightly reduced beginning stocks also decreased ending stocks. Despite the decline in ending stocks for both crops, USDA shaved a dime off its forecast average farm price, bringing the price for corn and soybeans to $4.30/bu. and $11.10/bu., respectively. Soybean meal prices remained unchanged at $330/ton.

While these forecasts suggest that feed costs should remain moderate, weather challenges are creating new supply concerns. Intense flooding in the Midwest and along the Mississippi river has damaged crop production with some analysts estimating that up to one million acres of corn could be lost with little hope that this acreage could be replanted.

Comments