Milk, Dairy and Grain Market Commentary

- Sarina Sharp

- Mar 7

- 4 min read

By Sarina Sharp, Daily Dairy Report

Milk, Dairy & Grain Markets

Like a teenager in a bad relationship, U.S. tariffs on goods from Canada and Mexico are on-again, off-again, and then changing their status to “it’s complicated.” The commodity and equity markets are like the teenager’s parents, reluctantly pulled into the emotional ups and downs, and desperately trying to restore calm. But this week it was all drama.

The situation may have changed by the time you read this, but for now, here’s the status of the relationship: The U.S. will not impose tariffs on goods covered under the U.S.-Mexico-Canada Agreement (USMCA). However, while most agricultural and auto-industry goods will be protected from tariffs through their USMCA status, many businesses had opted out of the complicated and expensive process of certifying that their products are USMCA-compliant. Those goods will now be subject to the zero- or low-tariff rates already in place before the trade spat plus the new 25% tariff. Trade Partnership Worldwide estimates that about 40% of U.S. imports from Canada and Mexico were not officially certified as USMCA compliant but crossed the border duty-free, and they’ll now face a 25% markup. An additional 22% of Canadian exports and 10% of Mexican imports paid small tariffs in the past and will now face a much larger border tax. It’s unclear whether the exemption for USMCA-compliant goods is a permanent pass, as stated in the Executive Order, or merely a pause until April 2, as stated repeatedly by members of the Trump administration. In early April, the Trump administration will also impose “reciprocal tariffs” on goods from the rest of the world. The U.S. now levies tariffs on Chinese imports that are 20% higher than they were in January, and China will begin taxing U.S. dairy imports – excluding dry whey and lactose – at a 10% markup from previous tariff levels.

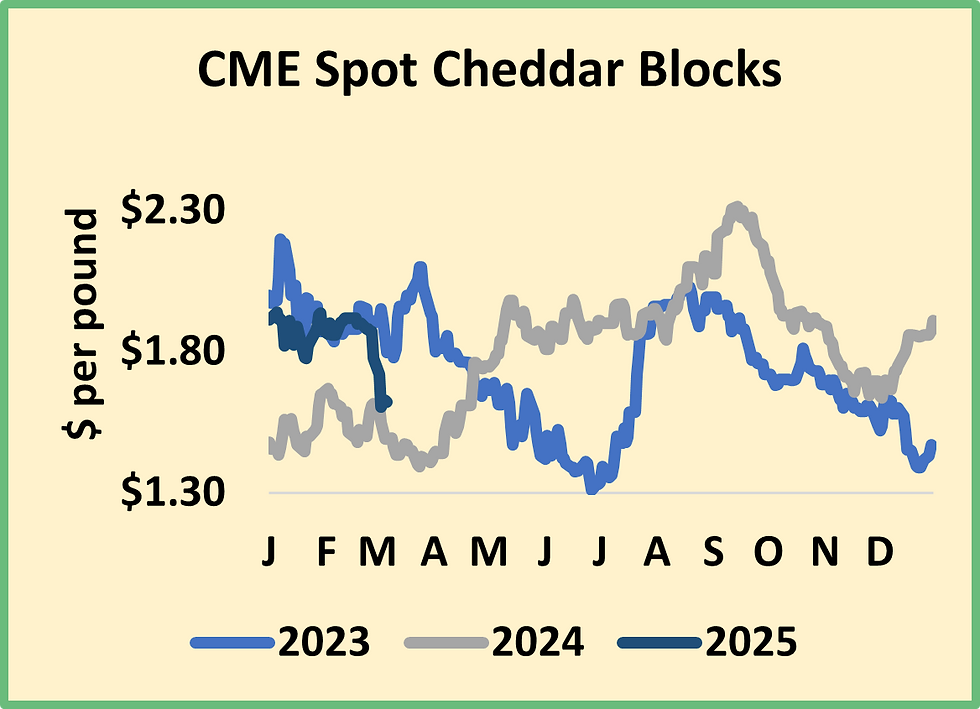

The back-and-forth on U.S. trade policy and a well-supplied milk market weighed heavily on U.S. dairy values this week. The bears were particularly bold in the cheese markets. CME spot Cheddar blocks plunged to an 11-month low at $1.6050 on Tuesday, but they clawed their way back to $1.6225 per pound, still down 15.25ȼ for the week. Barrels fell 15ȼ to $1.63.

This week’s dairy data was relatively friendly for cheese. U.S. cheese output reached 1.2 billion pounds in January, up 0.8% from the year before. But, once again, manufacturers focused on Mozzarella output. Cheddar production fell 1.4% year over year to the lowest January tally since 2020. That could limit the volume of cheese available for delivery in Chicago in the near term. Meanwhile, exports boomed. The U.S. sent nearly 100 million pounds of cheese abroad in January, 22% more than in January 2024. But the forward-looking futures market is anxious about new cheese capacity, slowing consumer demand, and the impacts of a potential trade war.

Thanks to higher components, there is simply too much cream. The glut has dragged down cream multiples to their lowest levels since the dark days of 2020. Class II manufacturers took advantage of cheap cream in January, making 20% more hard ice cream, 18% more full-fat cottage cheese, 5.3% more yogurt, and 4.3% more sour cream than they did the year before. But there was still enough cream left over to allow for a 0.5% uptick in butter output. U.S. butter is extremely cheap, which spurred a big jump in U.S. butter and cream exports in January. But there’s still more than enough butter around. On Tuesday CME spot butter regressed to $2.25, its lowest price since 2021. It closed today at $2.31, down 3.5ȼ for the week.

Powder prices continued to drop. CME spot nonfat dry milk (NDM) fell 4.5ȼ this week to a nine-month low at $1.155. Combined production of NDM and skim milk powder (SMP) totaled 189 million pounds, down 3.2% year over year and the lowest January output since 2016. Manufacturers showed a strong preference for NDM, which is primarily sold domestically or to buyers in Mexico. SMP production dropped 37.6% from January 2024, reflecting concerns that U.S. milk powder would fail to compete in foreign markets. That appears to be the right strategy. U.S. milk powder exports slowed to a crawl in January, falling below 100 million pounds for the first time in over five years. Shipments to Mexico topped January 2024, but powder exports to Southeast Asia hit eight-year lows in December 2024 and January 2025. Milk powder that might have gone to the Philippines or Vietnam went into storage instead. U.S. milk powder stocks jumped to nearly 300 million pounds, their highest level since May 2023.

To meet consumers’ appetite for protein, manufacturers made 20% more whey protein isolates (WPIs) in January than they did the year before, when WPI output was already running hot. That left less whey for whey protein concentrates (WPCs) and powder. Dry whey output fell 10.3% from year-ago levels.

Whey powder stocks grew slightly from December to January but remained well below January 2024 volumes. Whey powder exports topped January 2024 shipments, and almost half of them went to China. The steep drop in whey prices could encourage greater exports going forward. China was careful to exempt whey powder from its 10% retaliatory tariff on U.S. dairy products. However, China will exact a higher border tax on imports of U.S. WPIs and WPCs. American WPI and WPC values will have to retreat to offset the tariffs or lose market share to Germany. Spot whey powder prices lost ground again this week. They closed at an eight-month low of 49ȼ, down 2ȼ since last Friday.

The red ink flowed directly from the spot market to milk futures. April Class III plummeted more than a dollar to $17.21 per cwt. Most other Class III contracts suffered double-digit losses and settled in the $17s and $18s. Class IV futures lost around 30ȼ. While most contracts held well above the $18 mark, June Class IV closed at $17.93. Dairy profit margins are fading quickly.

Grain Markets

The feed markets went in circles this week. Volatility reigned, but May corn and soybeans finished right where they started, at $4.69 and $10.25 per bushel, respectively. Soybean meal rallied $4.50 to $304.50 per ton. U.S. soybean meal demand likely surged temporarily due to the brief tariff on canola imports. soybean futures a boost. But with big inventories from last year’s harvest, another massive Brazilian harvest on the horizon, and the threat of a trade war with some of our most important foreign buyers, feed prices are likely to languish.

Comments